Essential Valuation Metrics for Fundamental Investors

Understanding Valuation Fundamentals

For fundamental investors, understanding a company's intrinsic value is paramount. This value represents the true economic worth of a business, independent of its current market price. The disparity between intrinsic value and market price often signals investment opportunities. Valuation metrics serve as the quantitative tools to bridge this gap, offering a structured approach to evaluate a company's financial health, operational performance, and future potential. These metrics are not merely numbers; they are powerful indicators that, when analyzed contextually, reveal the underlying strengths and weaknesses of an enterprise.

Fundamental analysis, at its core, involves scrutinizing financial statements, management quality, industry trends, and macroeconomic factors to derive this intrinsic value. Valuation metrics simplify this complex process by distilling vast amounts of financial data into actionable ratios. However, no single metric provides a complete picture. A holistic approach, combining various ratios and qualitative insights, is essential for a comprehensive assessment.

What are Valuation Metrics?

Valuation metrics are financial ratios and indicators derived from a company's publicly available financial statements. They provide a standardized way to compare companies within the same industry or across different sectors, and to evaluate a single company's performance over time. These metrics help investors answer critical questions: Is the company profitable relative to its price? Is it efficiently using its assets? Is its debt manageable? Is its growth sustainable?

Different metrics are suited for different industries and business models. For instance, a technology company might be valued differently than a utility company, given their disparate asset structures, growth profiles, and risk exposures. A deep understanding of each metric's application and limitations is crucial for accurate interpretation.

Why Fundamental Investors Rely on Valuation

Fundamental investors adopt a long-term perspective, focusing on the underlying business rather than speculative market movements. Their objective is to acquire ownership in quality businesses at reasonable prices. Valuation metrics enable this by:

- Identifying Mispricings: Helping detect stocks that are trading below their intrinsic value, offering potential for capital appreciation.

- Risk Management: Highlighting companies with excessive debt, poor profitability, or unsustainable growth, thus mitigating investment risk.

- Comparative Analysis: Facilitating 'apples-to-apples' comparisons between competitors, even if they operate on different scales.

- Performance Tracking: Allowing investors to monitor a company's financial performance and valuation trends over time, ensuring it remains a viable investment.

- Capital Allocation: Informing decisions on where to allocate capital to maximize returns based on fundamental strength.

Without a rigorous valuation framework, investment decisions risk becoming speculative bets. By integrating these metrics, investors build a robust, evidence-based foundation for their portfolio choices.

Core Income-Based Valuation Ratios

Income-based valuation ratios relate a company's market capitalization or enterprise value to its earnings or sales. These metrics are among the most commonly used due to their straightforward calculation and direct link to a company's profitability.

Price-to-Earnings (P/E) Ratio

The Price-to-Earnings (P/E) Ratio is arguably the most recognized valuation metric. It expresses the relationship between a company's stock price and its earnings per share (EPS).

P/E Ratio = Market Price Per Share / Earnings Per Share (EPS)

A high P/E ratio typically suggests that investors expect higher earnings growth in the future, or that the company is perceived as a lower-risk investment. Conversely, a low P/E ratio might indicate an undervalued company, a company in decline, or a company with slower growth prospects. It's crucial to compare a company's P/E to its industry peers and its historical average to draw meaningful conclusions. The P/E ratio can be calculated using either trailing earnings (from the last 12 months) or forward earnings (analysts' estimates for the next 12 months).

PEG Ratio (Price/Earnings-to-Growth)

The PEG Ratio refines the P/E ratio by incorporating a company's expected earnings growth rate. It helps determine if a high P/E is justified by strong growth prospects.

PEG Ratio = P/E Ratio / Annual EPS Growth Rate

A PEG ratio of 1 is often considered fair value, suggesting the P/E ratio aligns with the growth rate. A PEG below 1 might indicate undervaluation, while a PEG above 1 could suggest overvaluation, assuming the growth rate is sustainable. This metric is particularly useful for growth-oriented companies where a high P/E might otherwise appear concerning.

Price-to-Sales (P/S) Ratio

The Price-to-Sales (P/S) Ratio compares a company's market capitalization to its total revenue over the last 12 months. It is particularly useful for valuing companies that may not yet be profitable, such as startups or companies in turnaround situations.

P/S Ratio = Market Capitalization / Total Revenue

A low P/S ratio can indicate an undervalued company, especially if it's operating in a high-growth industry with strong future profitability potential. However, a high P/S ratio for an unprofitable company warrants caution. This metric is less susceptible to accounting manipulations than earnings-based ratios but does not account for a company's cost structure or profitability.

Dividend Yield

While not a pure valuation metric in the same vein as P/E or P/S, Dividend Yield is critical for income-focused fundamental investors. It expresses the annual dividends per share as a percentage of the stock's current share price.

Dividend Yield = Annual Dividends Per Share / Market Price Per Share

A higher dividend yield typically appeals to investors seeking regular income. However, a very high yield could also signal that the market expects a dividend cut or that the stock price has fallen significantly due to underlying issues. Investors often analyze dividend yield in conjunction with the dividend payout ratio to assess the sustainability of dividend payments.

Asset-Based and Book Value Metrics

These metrics focus on a company's assets and liabilities, providing insights into its balance sheet strength and how the market values its tangible and intangible assets. They are especially relevant for capital-intensive industries or companies nearing liquidation.

Price-to-Book (P/B) Ratio

The Price-to-Book (P/B) Ratio compares a company's market capitalization to its book value of equity, which is total assets minus total liabilities.

P/B Ratio = Market Price Per Share / Book Value Per Share

A P/B ratio below 1 can indicate that the market values the company less than its net asset value, potentially signaling undervaluation, especially for companies with significant tangible assets. A high P/B ratio suggests the market attributes substantial value to the company's intangible assets, growth prospects, or strong brand. This metric is less effective for service-based companies with minimal physical assets but is highly relevant for banks, insurance companies, and manufacturing firms.

Tangible Book Value per Share

Tangible Book Value per Share refines the P/B ratio by excluding intangible assets (like goodwill, patents, and trademarks) from the calculation of book value. This provides a more conservative measure of a company's asset backing.

Tangible Book Value Per Share = (Total Assets - Intangible Assets - Total Liabilities) / Shares Outstanding

This metric is particularly useful for investors concerned about the quality of a company's assets or when evaluating companies where intangible assets might be overstated or difficult to value accurately. It offers a 'worst-case scenario' perspective on a company's liquidation value.

Enterprise Value and Cash Flow Metrics

Enterprise value (EV) metrics offer a more comprehensive view of a company's total value, including debt, which is particularly useful for acquisition analysis. Cash flow metrics, on the other hand, focus on a company's ability to generate actual cash, which is fundamental to its survival and growth.

Enterprise Value to EBITDA (EV/EBITDA)

The Enterprise Value to EBITDA (EV/EBITDA) ratio is a popular valuation multiple that compares a company's total value (including debt) to its earnings before interest, taxes, depreciation, and amortization.

EV/EBITDA = Enterprise Value / EBITDA

Enterprise Value (EV) is calculated as: Market Capitalization + Total Debt - Cash and Cash Equivalents. EBITDA is often used as a proxy for operating cash flow. EV/EBITDA is advantageous because it allows for direct comparison of companies with different capital structures, tax rates, and depreciation policies. It's widely used in industries with significant capital expenditures, such as manufacturing, telecommunications, and utilities. A lower EV/EBITDA typically suggests a more attractive valuation.

Enterprise Value to Sales (EV/Sales)

Similar to the P/S ratio, Enterprise Value to Sales (EV/Sales) compares a company's enterprise value to its total revenue. It shares the benefit of being applicable to unprofitable companies but accounts for debt and cash, offering a more complete picture of the company's value.

EV/Sales = Enterprise Value / Total Revenue

This metric is especially useful for early-stage or high-growth companies that are prioritizing revenue growth over immediate profitability. It helps investors assess how much value the market places on each dollar of a company's sales, taking its entire capital structure into account.

Price-to-Free Cash Flow (P/FCF)

The Price-to-Free Cash Flow (P/FCF) Ratio relates a company's market capitalization to its free cash flow (FCF). Free cash flow represents the cash a company generates after accounting for cash outflows to support operations and maintain its capital assets. It's a critical measure of financial health, as FCF can be used for debt repayment, dividends, share buybacks, or future investments.

P/FCF Ratio = Market Capitalization / Free Cash Flow

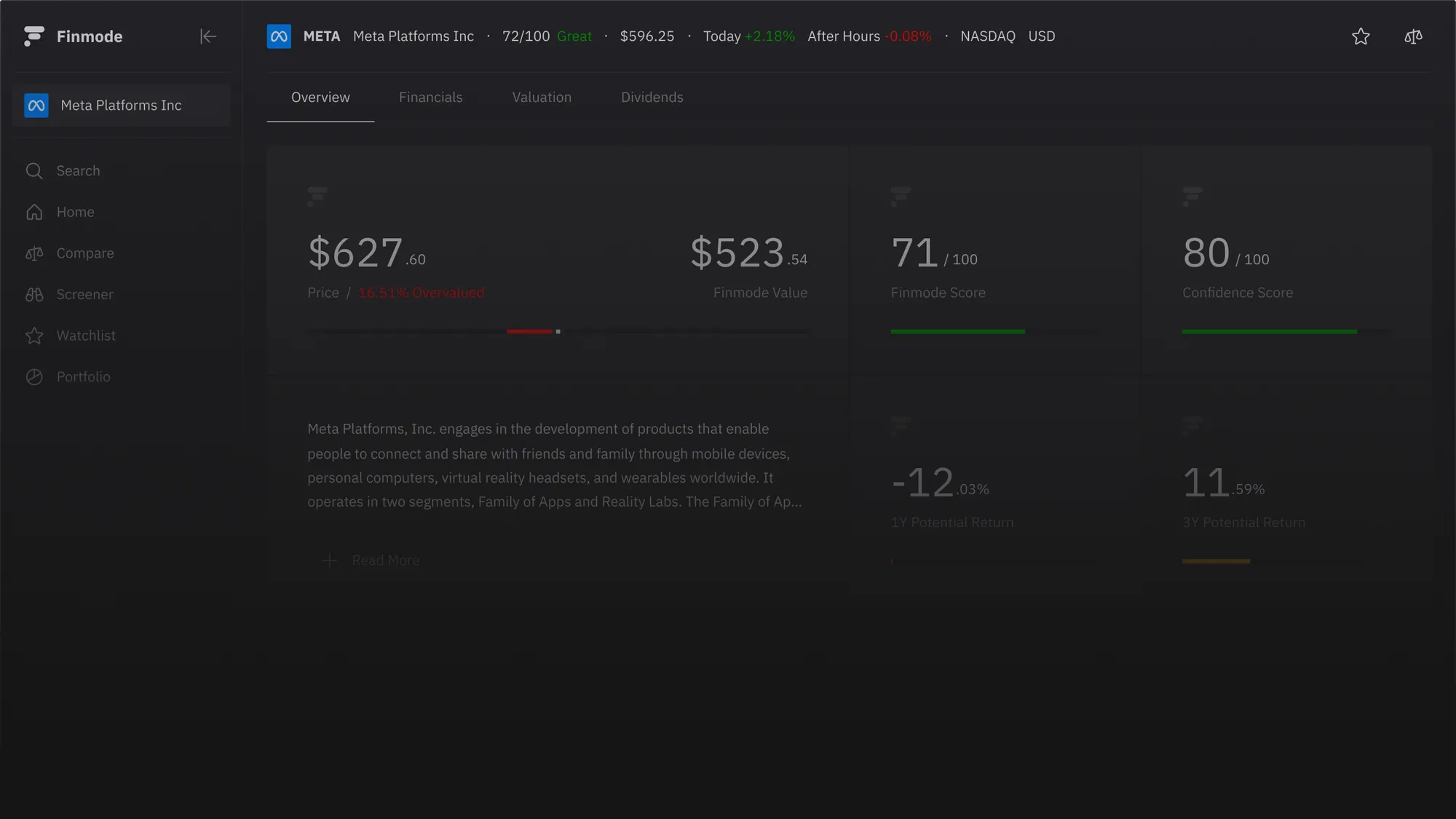

A lower P/FCF ratio suggests that a company is generating a substantial amount of cash relative to its market value, which can indicate undervaluation. This metric is highly regarded by fundamental investors because cash flow is less susceptible to accounting manipulations than earnings. Investors using finmode.app can easily track and compare FCF trends across different companies to identify those with robust cash generation capabilities. For a deeper dive into methods that incorporate free cash flow, consider exploring discounted cash flow analysis.

Discounted Cash Flow (DCF) Analysis: A Deeper Dive

While the ratios discussed above provide quick snapshots, Discounted Cash Flow (DCF) Analysis is a more sophisticated, intrinsic valuation method. DCF seeks to determine the value of an investment based on its future cash flows, discounted back to their present value. It's often considered the gold standard of valuation because it directly estimates the intrinsic value of a business based on its expected cash generation.

The process involves projecting a company's free cash flows for a specific period (typically 5-10 years) and then estimating a terminal value for all cash flows beyond that period. These future cash flows are then discounted back to the present using a discount rate, often the Weighted Average Cost of Capital (WACC), which represents the required rate of return for investors. While more complex and reliant on assumptions, DCF offers a granular view of a company's value drivers.

Relative Valuation: Benchmarking Companies

Beyond intrinsic valuation, fundamental investors heavily rely on relative valuation. This approach involves comparing a target company to similar companies (peers) in the same industry or sector, using common valuation multiples. The premise is that similar assets should trade at similar prices.

When performing relative valuation, analysts typically:

- Identify a peer group of comparable companies.

- Calculate various valuation multiples (P/E, P/B, EV/EBITDA, etc.) for each company in the peer group.

- Adjust for differences in growth rates, risk profiles, business models, and other factors.

- Apply the average or median multiple from the peer group to the target company's relevant financial metric (e.g., earnings, sales, EBITDA) to arrive at a valuation.

Relative valuation provides a market-based perspective, complementing the intrinsic value derived from methods like DCF. It helps contextualize whether a company's valuation is reasonable compared to its competitors. Effective relative valuation requires comprehensive financial statement analysis to ensure true comparability.

The Role of Growth and Risk in Valuation

No valuation metric exists in a vacuum. Two critical factors that profoundly influence valuation are growth and risk.

- Growth: Companies with higher sustainable growth prospects typically command higher valuation multiples. This is because future earnings and cash flows are expected to be larger, increasing their present value. However, investors must differentiate between sustainable, high-quality growth and speculative, debt-fueled expansion.

- Risk: Higher risk—whether operational, financial, industry-specific, or macroeconomic—justifies lower valuation multiples. Investors demand a higher return for taking on more risk, which translates to a lower price paid today for a given level of earnings or cash flow. Factors like competitive intensity, regulatory environment, balance sheet leverage, and management quality all contribute to a company's risk profile. Understanding economic moats and competitive advantages is crucial for assessing long-term risk.

A sophisticated fundamental investor incorporates these qualitative assessments into their quantitative valuation models, recognizing that a company's future is not merely a linear projection of its past performance.

Applying Valuation Metrics with finmode.app

Utilizing a comprehensive suite of valuation metrics effectively requires access to accurate, up-to-date financial data and robust analytical tools. This is where platforms like finmode.app prove invaluable for fundamental investors.

finmode.app provides streamlined access to financial statements, key ratios, and customizable screening tools that enable investors to:

- Quickly Calculate Ratios: Instantly access calculated P/E, P/B, EV/EBITDA, P/FCF, and many other metrics for thousands of companies.

- Perform Peer Comparisons: Easily compare a company's valuation multiples against its industry peers and historical averages, facilitating relative valuation analysis.

- Identify Investment Opportunities: Use advanced filters to screen for companies meeting specific valuation criteria, such as low P/E ratios coupled with strong growth or high free cash flow generation.

- Track Trends: Monitor how valuation multiples change over time for specific companies or entire sectors, providing context for current valuations.

By centralizing these analytical capabilities, finmode.app empowers fundamental investors to conduct thorough due diligence efficiently, moving beyond superficial analysis to uncover deeply researched investment opportunities.

Limitations and Nuances of Valuation Metrics

While powerful, valuation metrics are not without limitations. Investors must be aware of these nuances to avoid misinterpretations:

- Industry Specificity: What constitutes a 'good' P/E ratio in one industry might be unacceptable in another. Comparisons should primarily be within the same industry or with companies having similar business models.

- Accounting Practices: Differences in accounting policies (e.g., depreciation methods, revenue recognition) can distort ratios, making direct comparisons challenging. Investors must understand the underlying accounting choices.

- Qualitative Factors: Metrics do not capture qualitative aspects like management quality, brand strength, innovation potential, or competitive advantages. These non-financial factors are crucial for long-term success.

- Cyclicality: For cyclical industries, earnings and cash flows can fluctuate wildly, making P/E or P/FCF ratios highly volatile and less reliable during peak or trough periods.

- One-Time Events: Extraordinary gains or losses can artificially inflate or depress earnings, impacting P/E and other income-based ratios. Adjusting for these non-recurring items is often necessary.

- Growth Assumptions: Future growth rates used in PEG or DCF models are estimates and inherently uncertain. Overly optimistic growth projections can lead to overvaluation.

A sophisticated investor always uses a combination of metrics, qualitative analysis, and a critical eye, recognizing that no single number tells the whole story.

Conclusion: A Holistic Approach to Investment

Valuation metrics are indispensable tools for fundamental investors, offering quantitative insights into a company's financial health, operational efficiency, and market perception. From the widely used P/E ratio to the more comprehensive EV/EBITDA and the intrinsic DCF analysis, each metric provides a unique lens through which to examine an investment opportunity. However, their true power lies not in isolation, but in their synergistic application.

A successful fundamental investing strategy integrates a diverse array of valuation metrics with a thorough understanding of qualitative factors—such as management competence, industry dynamics, and competitive moats. By adopting a holistic, multi-faceted approach, investors can move beyond surface-level analysis, identify genuinely undervalued assets, and construct robust portfolios designed for long-term value creation. Continuous learning and adaptation to market nuances remain key to mastering the art and science of valuation.

Frequently Asked Questions

What is the primary purpose of valuation metrics?

The primary purpose of valuation metrics is to quantitatively assess a company's intrinsic value and determine if its market price reflects that value. They help fundamental investors identify whether a stock is undervalued or overvalued by comparing financial performance and assets to its current share price.

How do P/E and EV/EBITDA differ in application?

The P/E ratio relates a company's stock price to its earnings per share, focusing on equity value and profitability for shareholders. EV/EBITDA, conversely, compares a company's total enterprise value (market cap plus debt minus cash) to its operating earnings before non-cash expenses, providing a capital-structure-neutral view useful for comparing companies with different financing models or capital intensities.

Why is relative valuation important?

Relative valuation is crucial because it provides a market-based context for a company's worth by comparing it to similar businesses in the same industry. This helps investors determine if a company's valuation multiples are reasonable or an outlier when benchmarked against its peers, enhancing the decision-making process.

Can valuation metrics predict future stock prices?

Valuation metrics do not directly predict future stock prices; rather, they help investors estimate a company's intrinsic value today. While identifying undervalued companies based on these metrics suggests potential for future price appreciation, actual stock movements are influenced by numerous factors, including market sentiment, economic conditions, and unforeseen events, making direct prediction impossible.

Read more insights

Try Finmode Today

Free To Get Started

While we strive to provide accurate and reliable information, the content provided on this platform is for informational purposes only and should not be construed as financial advice. The information contained herein is based on data and analysis that we believe to be accurate and reliable, but it is not guaranteed to be complete or error-free.

No Investment Advice:

The information provided does not constitute a recommendation to buy, sell, or hold any security. Any decision to invest in any security should be made based on your own research and analysis, or with the assistance of a qualified financial advisor.

Risk of Loss:

Investing in stocks involves significant risk, including the potential for loss of principal. Past performance is not indicative of future results.No

Warranty:

We make no warranties, expressed or implied, as to the accuracy, completeness, or reliability of the information provided. We are not liable for any losses or damages, direct or indirect, arising from the use or reliance on the information provided.

User Responsibility:

It is your sole responsibility to evaluate the accuracy, completeness, and reliability of the information provided and to make your own investment decisions.

FINMODE S.R.L - DOGLIANI (CN) PIAZZA VITTORIO GRASSO 12 - P.IVA 04164500045 - N.REA CN - 340581 - CAP. SOCIALE 15000€