Mastering Financial Statements for Fundamental Investing

The Pillars of Financial Analysis: Income, Balance, Cash Flow

For fundamental investors, financial statements serve as the primary lens through which a company's economic reality is understood. These standardized reports offer a comprehensive view of a business's past performance and current position, enabling sophisticated analysis beyond superficial metrics. Understanding each statement individually, and more importantly, their symbiotic relationship, is non-negotiable for anyone aspiring to make data-driven investment decisions.

The Income Statement: Performance Over Time

The income statement, also known as the profit and loss (P&L) statement, details a company's revenues, expenses, and ultimately its net income or loss over a specific period, typically a quarter or a year. It provides insights into a company's operational profitability and its ability to convert sales into earnings. Key components include revenue, representing the total sales generated; cost of goods sold (COGS), the direct costs attributable to producing the goods or services sold; and gross profit, which is revenue minus COGS. Further down, operating expenses like selling, general, and administrative (SG&A) expenses and research and development (R&D) are deducted to arrive at operating income (EBIT). After accounting for interest and taxes, the final figure is net income, which is the profit available to shareholders.

Investors analyze the income statement to track revenue growth, margin expansion or contraction, and expense management. Consistent revenue growth, coupled with stable or improving gross and net profit margins, often signals a healthy and competitive business. Conversely, declining revenues or eroding margins can indicate competitive pressures, operational inefficiencies, or a weakening market position. Understanding the drivers behind these trends is crucial; for instance, a temporary spike in expenses might be a strategic investment rather than a structural issue. Fundamental investors also look at non-recurring items or extraordinary gains/losses that can distort the true operational profitability, adjusting the reported net income for a clearer picture.

The Balance Sheet: A Snapshot of Financial Health

The balance sheet provides a snapshot of a company's financial position at a specific point in time. It adheres to the fundamental accounting equation: Assets = Liabilities + Shareholder's Equity. This statement reveals what a company owns (assets), what it owes (liabilities), and the residual value belonging to its owners (equity). Assets are categorized as current assets (cash, accounts receivable, inventory) which can be converted to cash within one year, and non-current assets (property, plant, equipment, intangible assets) which have a longer-term benefit. Liabilities are similarly split into current liabilities (accounts payable, short-term debt) due within one year, and non-current liabilities (long-term debt, deferred tax liabilities).

The balance sheet is vital for assessing a company's liquidity (ability to meet short-term obligations) and solvency (ability to meet long-term obligations). A strong balance sheet typically features ample cash, manageable debt levels, and significant shareholder equity. High levels of debt relative to equity can signal financial risk, especially if interest rates rise or economic conditions deteriorate. Analyzing the composition of assets also offers insights; for example, a company with a high proportion of intangible assets might be valued differently than one heavily reliant on physical plant and equipment. Changes in working capital (current assets minus current liabilities) can reveal operational efficiency improvements or deterioration.

The Cash Flow Statement: Understanding True Liquidity

While the income statement shows profitability and the balance sheet shows financial position, the cash flow statement reveals how much cash a company generates and uses over a period. This statement is often considered the most reliable indicator of a company's financial health because cash flows are less susceptible to accounting manipulations than earnings. It categorizes cash flows into three main sections: operating activities, investing activities, and financing activities.

Cash flow from operating activities represents cash generated from normal business operations. A consistently positive and growing operating cash flow is a strong indicator of a healthy business that can fund its operations without external financing. Cash flow from investing activities includes cash used for or generated from the purchase or sale of long-term assets, such as property, plant, and equipment, or investments in other companies. Significant cash outflows here can indicate strategic investments for future growth, while inflows might suggest asset sales. Cash flow from financing activities includes cash transactions related to debt, equity, and dividends. This includes issuing or repurchasing stock, borrowing or repaying loans, and paying dividends to shareholders.

A critical metric derived from the cash flow statement is free cash flow (FCF), which is the cash a company generates after accounting for cash outflows to support its operations and maintain its capital assets. FCF is the cash available to distribute to creditors and shareholders, make acquisitions, or pay down debt. Companies with strong, consistent FCF are often highly attractive to fundamental investors, as it signifies financial flexibility and the capacity for sustainable value creation. Understanding a company's true liquidity is significantly enhanced by a thorough understanding a company's true liquidity, which is best achieved through detailed cash flow analysis.

Key Ratios and Metrics for Fundamental Investors

Financial ratios normalize data from financial statements, allowing for meaningful comparisons across different companies and over time. These ratios provide quick insights into various aspects of a company's performance and financial health, helping fundamental investors to identify strengths, weaknesses, and potential red flags.

Profitability Ratios

These ratios assess a company's ability to generate earnings relative to its revenue, assets, or equity.

- Gross Profit Margin:

(Revenue - COGS) / Revenue. Indicates the percentage of revenue available to cover operating expenses and generate profit after accounting for direct production costs. A higher margin suggests efficient production or strong pricing power. - Net Profit Margin:

Net Income / Revenue. Reveals how much profit a company makes for every dollar of sales after all expenses, including taxes and interest, have been deducted. It's a key indicator of overall efficiency. - Return on Equity (ROE):

Net Income / Shareholder's Equity. Measures how much profit a company generates for each dollar of shareholder's equity. A higher ROE indicates efficient use of shareholder investments to generate profits. - Return on Assets (ROA):

Net Income / Total Assets. Shows how efficiently a company is using its assets to generate profits.

Liquidity and Solvency Ratios

These ratios evaluate a company's ability to meet its short-term and long-term financial obligations.

- Current Ratio:

Current Assets / Current Liabilities. Measures a company's ability to cover its short-term debts with its short-term assets. A ratio of 2.0 or higher is generally considered healthy, though this varies by industry. - Quick Ratio (Acid-Test Ratio):

(Current Assets - Inventory) / Current Liabilities. A more conservative measure than the current ratio, as it excludes inventory, which might not be easily convertible to cash. - Debt-to-Equity Ratio:

Total Debt / Shareholder's Equity. Indicates the proportion of a company's financing that comes from debt versus equity. A lower ratio generally implies less financial risk. - Interest Coverage Ratio:

EBIT / Interest Expense. Assesses a company's ability to pay interest on its outstanding debt. A higher ratio indicates a greater ability to meet interest obligations.

Efficiency Ratios

Efficiency ratios gauge how effectively a company is using its assets and managing its liabilities.

- Inventory Turnover:

Cost of Goods Sold / Average Inventory. Measures how many times inventory is sold and replaced over a period. A higher turnover can indicate efficient inventory management and strong sales, but too high might suggest insufficient inventory levels. - Days Sales Outstanding (DSO):

(Accounts Receivable / Revenue) * Number of Days in Period. Shows the average number of days it takes for a company to collect its accounts receivable. Lower DSO is generally better, indicating efficient credit and collection policies.

Valuation Ratios

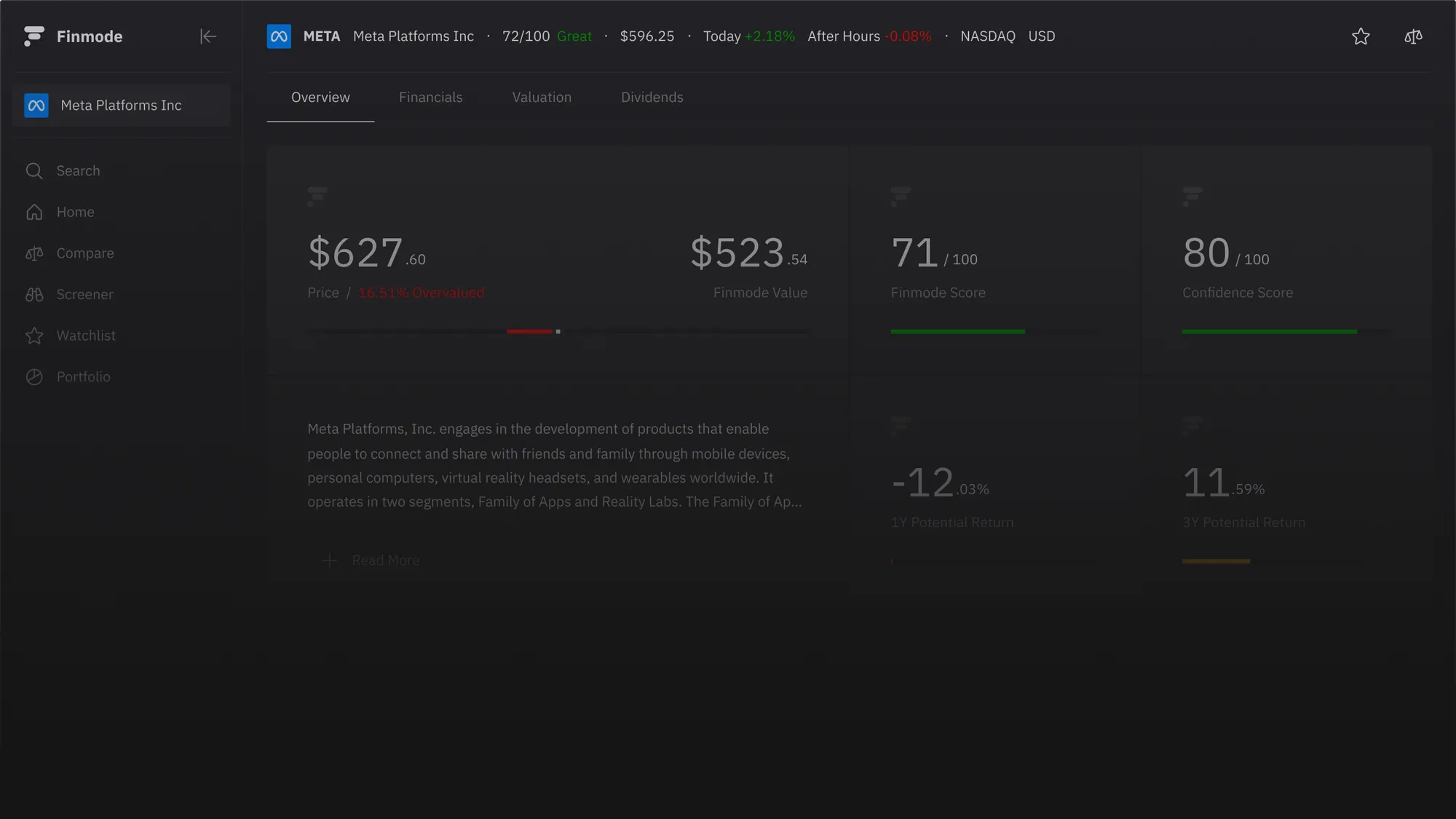

While often forward-looking and market-dependent, understanding interpreting various valuation multiples is essential for fundamental investors when contextualizing a company's market price against its financial performance. Ratios like Price-to-Earnings (P/E), Price-to-Book (P/B), and Enterprise Value-to-EBITDA (EV/EBITDA) are commonly used. Platforms like finmode.app provide investors with a comprehensive suite of these valuation metrics, allowing for quick comparisons and deeper insights into a company's market perception relative to its intrinsic value drivers.

Integrated Analysis: Connecting the Statements

Financial statements are not isolated documents; they are intricately linked, with changes in one impacting the others. A fundamental investor must understand these interconnections to paint a holistic picture of a company's financial story. For example, depreciation expense recorded on the income statement (reducing net income) also reduces the book value of assets on the balance sheet and is added back in the operating activities section of the cash flow statement (as it's a non-cash expense).

Consider the impact of a significant capital expenditure. On the balance sheet, Property, Plant, and Equipment (PP&E) increases, and cash decreases. On the cash flow statement, this appears as an outflow under investing activities. In subsequent periods, this asset will lead to depreciation expense on the income statement, reducing reported profits, but will not be a cash outflow. This dynamic interplay highlights the necessity of reviewing all three statements in conjunction, rather than in isolation.

The DuPont analysis is an excellent example of integrated analysis, breaking down Return on Equity (ROE) into three key components: net profit margin (income statement), asset turnover (income statement & balance sheet), and financial leverage (balance sheet). By disaggregating ROE, investors can pinpoint whether profitability is driven by strong margins, efficient asset utilization, or the use of debt, providing a nuanced understanding of performance drivers.

Common Pitfalls and Advanced Considerations

While financial statements provide invaluable data, their analysis is not without challenges. Fundamental investors must remain vigilant for potential distortions and understand the broader context in which a company operates.

Accounting Shenanigans and Red Flags

Companies can sometimes use aggressive accounting practices to present a more favorable financial picture. Identifying accounting red flags is a critical skill for investors. These can include premature revenue recognition, aggressive expense capitalization, manipulating reserves, or using complex off-balance sheet financing structures to hide debt. For example, a significant divergence between net income and operating cash flow over time can be a warning sign, as can a sudden increase in accounts receivable without a corresponding increase in revenue. Investors should also be wary of frequent changes in accounting policies or an overuse of non-GAAP (Generally Accepted Accounting Principles) metrics that exclude certain expenses.

Industry-Specific Nuances

Different industries have distinct financial characteristics and key performance indicators. For instance, inventory management is critical for retailers, while capital expenditure and depreciation are more dominant for manufacturing firms. Technology companies often have significant intangible assets and R&D expenses. Therefore, comparing ratios across different industries can be misleading. A thorough understanding of industry benchmarks and specific drivers is essential for accurate analysis. What constitutes a healthy debt-to-equity ratio in one sector might be considered excessive in another.

Qualitative Factors

Quantitative analysis of financial statements should always be complemented by qualitative assessment. Factors such as the quality and integrity of management, the strength of a company's competitive advantages (moat), industry trends, regulatory environment, and macroeconomic conditions can significantly influence a company's future performance, even if its current financials appear robust. A company with excellent financial statements but poor governance or an eroding competitive position may not be a sound long-term investment.

Leveraging Technology for Deeper Insights

The sheer volume of financial data available today can be overwhelming for individual investors. This is where modern fintech tools become indispensable. Platforms like finmode.app streamline the process of collecting, analyzing, and visualizing financial statement data, empowering fundamental investors with advanced capabilities.

finmode.app provides access to comprehensive historical financial data, allowing investors to quickly screen for companies based on specific criteria, analyze trend lines for revenues, profits, and cash flows, and compare key ratios against industry peers. Its intuitive interface transforms raw data into actionable insights, enabling users to identify potential investment opportunities or risks efficiently. For example, with finmode.app, an investor can easily track a company's ROE decomposition through DuPont analysis over several years or benchmark its gross profit margin against its top competitors, facilitating a more robust and timely investment analysis. By consolidating complex financial data into an intuitive interface, finmode.app empowers fundamental investors to perform efficient screening and in-depth analysis of key metrics, ensuring no critical detail is overlooked in their pursuit of intrinsic value.

Frequently Asked Questions

Read more insights

Try Finmode Today

Free To Get Started

While we strive to provide accurate and reliable information, the content provided on this platform is for informational purposes only and should not be construed as financial advice. The information contained herein is based on data and analysis that we believe to be accurate and reliable, but it is not guaranteed to be complete or error-free.

No Investment Advice:

The information provided does not constitute a recommendation to buy, sell, or hold any security. Any decision to invest in any security should be made based on your own research and analysis, or with the assistance of a qualified financial advisor.

Risk of Loss:

Investing in stocks involves significant risk, including the potential for loss of principal. Past performance is not indicative of future results.No

Warranty:

We make no warranties, expressed or implied, as to the accuracy, completeness, or reliability of the information provided. We are not liable for any losses or damages, direct or indirect, arising from the use or reliance on the information provided.

User Responsibility:

It is your sole responsibility to evaluate the accuracy, completeness, and reliability of the information provided and to make your own investment decisions.

FINMODE S.R.L - DOGLIANI (CN) PIAZZA VITTORIO GRASSO 12 - P.IVA 04164500045 - N.REA CN - 340581 - CAP. SOCIALE 15000€